The quick read

A plain-English guide to the State Bank of Pakistan releases scheduled for July 13–17, and how deposits, credit and external-sector data can change the way investors read the PSX.

One-sentence thesis

The next week’s scheduled State Bank of Pakistan releases will not predict PSX prices, but they can change how investors read bank funding, business borrowing, currency pressure and sector risk.

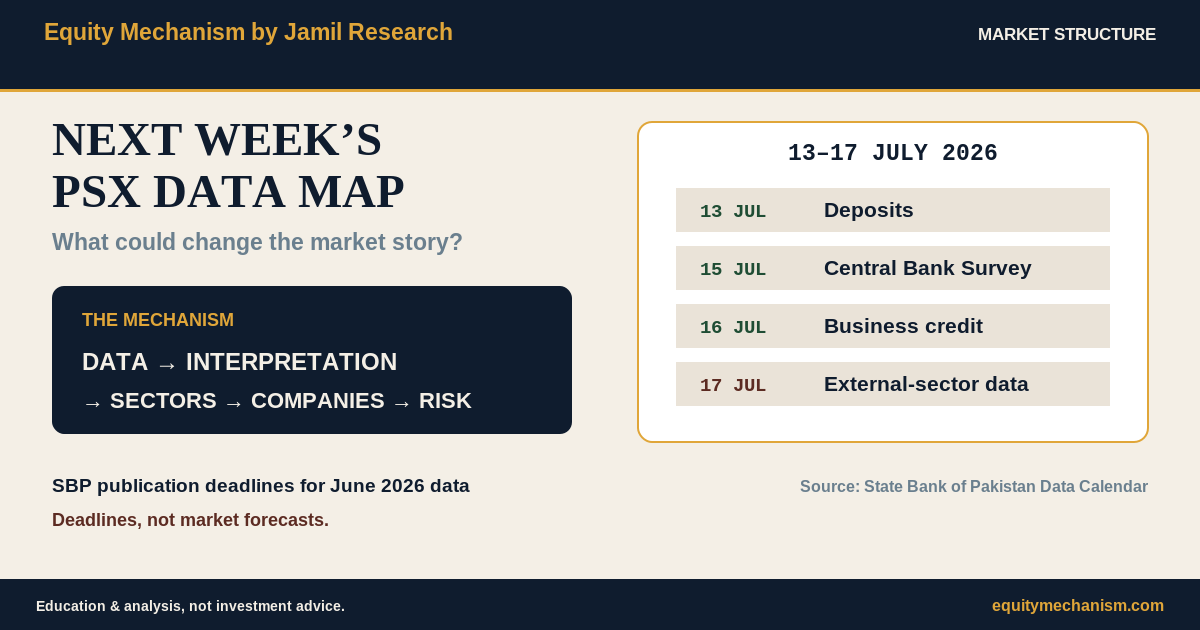

- The State Bank of Pakistan lists June deposit data for publication not later than July 13, 2026.

- The Central Bank Survey is listed not later than July 15.

- Three credit datasets are listed not later than July 16.

- A broad set of trade, foreign-investment, balance-of-payments and effective-exchange-rate datasets is listed not later than July 17.

- These are publication deadlines, not forecasts and not promises that every dataset will first appear on that exact day.

- The useful reading is not “good data” or “bad data.” It is: what changed, where it changed, and how that change can transmit into sectors and companies.

Start with the calendar, not a market prediction

A data calendar is useful because it tells investors when new evidence may become available.

It does not tell them whether the KSE-100 should rise or fall.

That distinction matters. A release can look supportive at the headline level but become less convincing when its composition is examined. The reverse can also happen: a weak total may contain an improving sub-category.

The State Bank of Pakistan describes the dates below as “Not Later Than” deadlines.

| Deadline | Scheduled June 2026 datasets | Main market question |

|---|---|---|

| July 13 | Deposits by holder category; foreign-currency deposits | Is bank funding changing, and how are savers positioned? |

| July 15 | Central Bank Survey | Are money and liquidity conditions changing? |

| July 16 | Advances and loans by security, borrower and finance type | Is business borrowing expanding, and where? |

| July 17 | Trade, foreign investment, balance of payments and effective exchange-rate indices | Is external pressure easing or building? |

The dates are verified facts. The market questions are analytical interpretation.

July 13: deposits and the quality of bank funding

The first group covers deposits distributed by holder category and foreign-currency deposits.

Deposits matter because they are a major source of bank funding. But the total is only the starting point.

A better reading asks:

- Which holder categories are adding deposits?

- Is the change concentrated in current accounts, savings behaviour or another segment?

- Are foreign-currency deposits rising or falling?

- Is deposit growth being translated into credit, investment in government securities, or simply higher liquidity?

A higher deposit total is not automatically positive for every bank. The cost and mix of funding matter. A bank can gather more deposits but still face pressure if those funds are expensive or if credit demand remains weak.

The market channel is:

deposit mix → funding conditions → liquidity and lending capacity → bank earnings questions

That is a mechanism, not a guaranteed result.

July 15: the Central Bank Survey and liquidity context

The Central Bank Survey is a monthly view of the State Bank of Pakistan’s balance sheet.

For a market reader, the useful categories include foreign assets, claims on government and liabilities to the banking system.

The survey can help answer whether liquidity conditions are changing and whether the central bank’s balance sheet is adding or absorbing pressure through different channels.

It should not be read as a single-number signal.

For example, a movement in foreign assets may matter for external liquidity, while a change in claims on government may carry a different fiscal and monetary meaning. A shift in liabilities can affect how the banking system’s position is interpreted.

The transmission path is:

central-bank balance sheet → money and liquidity conditions → rate expectations → banks and rate-sensitive sectors

The effect depends on direction, size, composition and persistence.

July 16: credit data and the location of business demand

The July 16 group includes:

- advances classified by securities and borrowers;

- credit or loans classified by borrowers; and

- loans to private-sector businesses by type of finance.

This is more useful than a single headline credit number because it helps locate borrowing demand.

Stronger private-sector borrowing can be consistent with business expansion, working-capital needs or investment. It may also support bank income if lending grows at reasonable pricing and credit quality remains sound.

But rising credit is not always evidence of broad expansion.

Borrowing can increase because firms need more working capital after costs rise. It can be concentrated in a few sectors. It can also create future credit-quality risk if borrowers are already under pressure.

The better questions are:

- Which borrowers took more credit?

- Was the increase short-term or longer-term?

- Which financing types grew?

- Did the movement appear broad or concentrated?

- Is credit growth consistent with other evidence of economic activity?

The mechanism is:

borrower demand → bank lending → business activity or cost pressure → sector and company impact

The same headline can therefore support more than one interpretation.

July 17: the external-sector data bundle

July 17 has the largest scheduled group.

It includes trade, export receipts, import payments, foreign direct investment, broader foreign-investment data, the summary of the balance of payments, seasonally adjusted balance-of-payments data, and nominal and real effective exchange-rate indices.

This matters because external pressure can reach listed companies through several routes:

- the Pakistani rupee;

- imported fuel, machinery and raw-material costs;

- export competitiveness;

- access to foreign financing;

- profit repatriation expectations; and

- the broader interest-rate outlook.

The balance of payments summarises transactions between Pakistan’s residents and non-residents. It is broader than the goods-trade balance alone.

The nominal effective exchange rate tracks the rupee against a basket of currencies. The real effective exchange rate adjusts that broad currency measure for relative prices.

These indices are useful context, but they should not be reduced to a simple “rupee is cheap” or “rupee is expensive” conclusion. Competitiveness depends on productivity, costs, trade structure and other factors as well.

The transmission path is:

trade, investment and external flows → currency and financing pressure → import costs and competitiveness → sector margins → company risk

Sector and company questions

The releases can affect sectors differently.

Banks

Watch deposit composition, credit demand and the balance between lending and other uses of funds.

Import-dependent manufacturers

Watch currency pressure and import-payment trends because raw materials, machinery and energy inputs can be dollar-linked.

Exporters

Watch export receipts, currency conditions and real competitiveness. A weaker rupee can support translated revenue, but imported inputs and domestic inflation can offset part of that benefit.

Energy and commodity-linked companies

Watch external financing, import payments and currency transmission into fuel and equipment costs.

Highly leveraged companies

Watch whether the data changes interest-rate expectations. The effect will depend on debt structure and refinancing timing.

These are screening questions. Company conclusions require company filings.

Verified fact versus named inference

Verified facts

- SBP lists deposit datasets not later than July 13.

- SBP lists the Central Bank Survey not later than July 15.

- SBP lists three credit datasets not later than July 16.

- SBP lists the main June trade, investment, balance-of-payments and effective-exchange-rate datasets not later than July 17.

- SBP uses “Not Later Than” wording.

Named inference

Inference: The releases may change how investors assess bank funding, liquidity, business demand, currency pressure, import costs and sector margins.

Why it is an inference: The data had not yet been released when this article was prepared. The direction, composition, revisions and persistence will determine the actual market relevance.

What would weaken the interpretation?

A single monthly release may be noisy.

The mechanism becomes less convincing if:

- one category improves while the broader picture weakens;

- the result is driven by a temporary or one-off item;

- later revisions materially change the reading;

- deposits rise but private-sector credit remains weak;

- the external balance improves only because imports fall during weak activity;

- foreign investment rises because of one transaction rather than a broad trend; or

- the market has already priced in the information.

Risk and falsifier

The main risk is over-interpreting one month.

A useful falsifier is:

If the July releases point in different directions and the following months do not confirm the same mechanism, the weekly narrative should not be treated as a durable trend.

Another falsifier is sector-specific:

If external indicators improve but import-dependent company margins do not, company pricing, inventory timing, energy use or operational issues may matter more than the macro channel.

What to watch after each release

- Direction: Did the number rise or fall?

- Composition: Which categories caused the change?

- Comparison: Is the move different from recent months?

- Revision: Were earlier figures changed?

- Transmission: Which sectors should theoretically feel the effect?

- Confirmation: Do company filings and later data support the same story?

The objective is not to turn every release into a trading signal.

The objective is to build a disciplined evidence chain:

data → interpretation → sector impact → company questions → risk

Sources

- State Bank of Pakistan: Data Calendar

- State Bank of Pakistan: Economic Data

- State Bank of Pakistan: Glossary of Key Economic Terms

- State Bank of Pakistan EasyData: Credit/Loans Classified by Borrowers

Source note: The publication dates and dataset names are taken from the SBP Data Calendar. The sector and market channels are named inference and are not guaranteed outcomes.

Education & analysis, not investment advice.

Falsifier

Update this analysis if the next primary-source data point contradicts the stated mechanism.

Next data point

Monitor the next official data release, company filing, PSX notice, or sector data point linked to this mechanism.