The quick read

Lucky Cement sold more cement locally in 1H FY26, but the stronger signal was that cost of sales stayed contained while operating efficiency improved.

One-sentence thesis

Lucky Cement's Pakistan cement margin widened because higher local activity was accompanied by contained cost of sales and operating-efficiency gains. Lower international coal benchmarks and a relatively orderly rupee were supportive context, but neither should be treated as a complete explanation on its own.

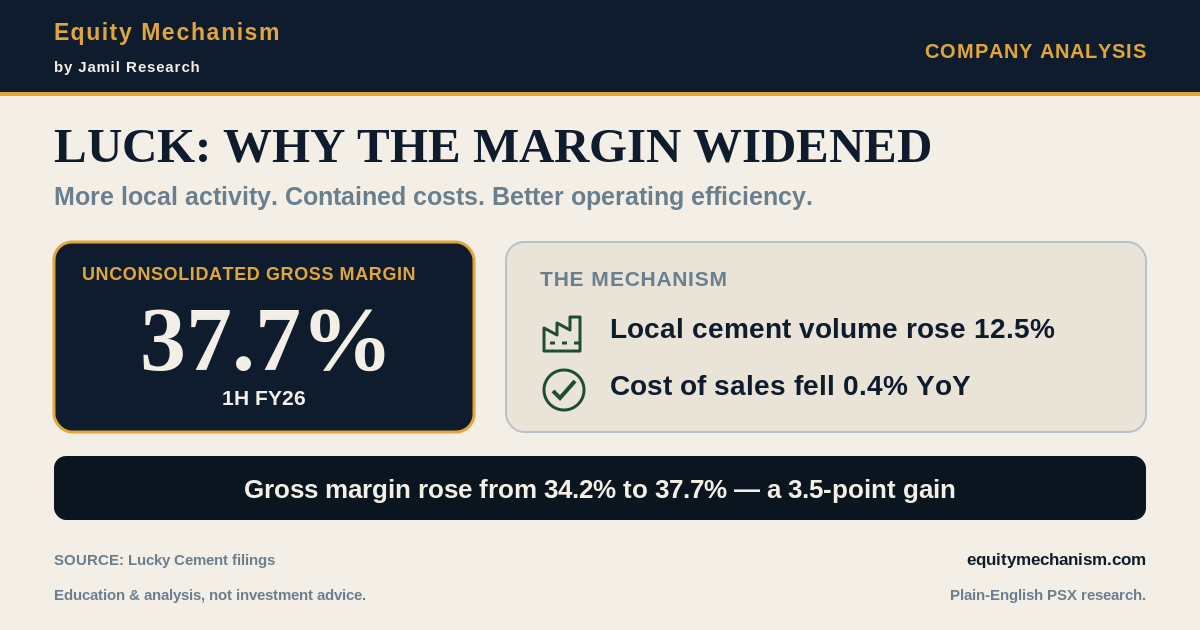

- LUCK's unconsolidated gross margin rose to 37.7% in 1H FY26 from 34.2% in 1H FY25, an improvement of 3.5 percentage points.

- Local cement volume increased about 12.5%, while cost of sales fell about 0.4% year on year.

- Lucky Cement said an orderly exchange rate reduced input-cost volatility.

- The company said UTIS technology on two Karachi lines reduced coal consumption, improved clinker output and lowered production costs.

- International coal prices provide useful direction, but they are not Lucky Cement's disclosed purchase cost.

- For the Pakistan cement operation, the unconsolidated accounts are a cleaner lens than the consolidated group accounts.

Start with the right accounts

Lucky Cement is more than a Pakistan cement producer. Its consolidated financial statements include businesses linked to automobiles, chemicals, power and other investments.

That wider group view is useful when studying the whole company, but it can blur the mechanism inside the domestic cement operation.

For the nine months ended March 2026:

| Reporting scope | Gross margin |

|---|---|

| Consolidated group | 24.8% |

| Unconsolidated company | 37.5% |

The two figures are not competing versions of the same number. They describe different scopes.

The consolidated margin blends several businesses. The unconsolidated margin is the cleaner starting point for analysing Lucky Cement's Pakistan cement operations.

Company snapshot

| Item | Reading |

|---|---|

| Company | Lucky Cement Limited |

| PSX ticker | LUCK |

| Primary lens in this article | Unconsolidated Pakistan cement operations |

| Main period studied | Six months ended December 31, 2025 |

| Confirmation period | Nine months ended March 31, 2026 |

| Core question | Why did gross margin widen? |

| Main disclosed supports | Higher local volume, contained costs, exchange-rate stability and UTIS efficiency |

| Important limitation | Realised coal purchase cost and a clean domestic retention price are not disclosed |

What changed in 1H FY26?

The headline movement was straightforward:

| Metric | 1H FY25 | 1H FY26 | Change |

|---|---|---|---|

| Unconsolidated gross margin | 34.2% | 37.7% | +3.5 percentage points |

| Local cement volume | — | — | +12.5% year on year |

| Cost of sales | — | — | -0.4% year on year |

Gross margin means gross profit as a share of net revenue.

A wider gross margin means the company retained more gross profit from each rupee of reported net revenue after accounting for cost of sales.

The important combination is this:

Local activity increased, but cost of sales did not rise with it.

That does not prove that every bag became cheaper to produce. It does show that the reported cost base stayed contained despite higher local volumes.

Financial-quality reading

| Question | Evidence | Reading |

|---|---|---|

| Did the company sell more locally? | Local cement volume rose about 12.5% | Yes |

| Did cost of sales rise with the additional activity? | Cost of sales fell about 0.4% | No |

| Did gross margin improve? | 37.7% versus 34.2% | Yes |

| Is coal the proven cause? | LUCK does not disclose its realised coal purchase price | No |

| Did the company disclose efficiency support? | UTIS reduced coal consumption and improved clinker output | Yes |

| Is the group margin the right cement lens? | Consolidated results include other businesses | No |

The mechanism

The margin improvement can be read through four linked channels.

1. Higher local volume supported activity

Local cement volumes rose about 12.5% year on year.

Higher production and sales can improve cost absorption because fixed operating costs are spread over more output. But volume alone does not guarantee a wider margin.

A company can sell more and still earn a weaker margin if fuel, power, freight or discounts rise faster than revenue.

The useful signal here is that Lucky Cement's local activity increased while cost of sales remained contained.

2. An orderly rupee reduced input-cost volatility

Cement production relies on imported or dollar-linked inputs, directly or indirectly.

When the Pakistani rupee weakens sharply, the local-currency cost of imported fuel, spare parts and equipment can rise even if international prices are unchanged.

Lucky Cement said the exchange-rate environment was orderly during the period and reduced volatility in input costs.

That does not mean foreign-exchange risk disappeared. It means the currency did not create the same level of additional cost pressure that a sharp depreciation could have caused.

3. UTIS improved operating efficiency

Lucky Cement disclosed that UTIS technology was operating on two of four Karachi production lines.

According to the company, the system:

- reduced coal consumption;

- improved clinker output; and

- lowered production costs.

This is important because it represents a company-specific operating change, not merely an external commodity-price movement.

The company expected the remaining two Karachi lines to be commissioned during 4Q FY26. Confirmation of that rollout matters because it may show whether the efficiency benefit can extend across more of the production base.

4. Lower coal benchmarks were a possible tailwind

Coal is a major fuel input in cement production.

The International Energy Agency reported that Newcastle free-on-board coal with a calorific value of 6,000 kcal/kg averaged about USD104 per tonne in calendar 2025, down 22% from 2024.

That provides useful market direction, but it must be handled carefully.

The benchmark is:

- not Lucky Cement's disclosed purchase price;

- not adjusted for LUCK's coal grade or supplier mix;

- not adjusted for freight, duties or inventory timing; and

- based on calendar 2025, which does not exactly match LUCK's fiscal reporting periods.

Therefore, lower coal benchmarks may have supported the cost environment, but they do not independently prove how much Lucky Cement saved.

Verified fact versus named inference

Verified facts

- Unconsolidated gross margin rose from 34.2% to 37.7% in 1H FY26.

- Local cement volume increased about 12.5%.

- Cost of sales declined about 0.4%.

- Lucky Cement said an orderly exchange rate reduced input-cost volatility.

- Lucky Cement said UTIS reduced coal consumption, improved clinker output and lowered production costs.

- The nine-month unconsolidated gross margin was 37.5%, compared with 24.8% on a consolidated basis.

Named inference

Inference: The combination of higher local activity and contained cost of sales suggests that cost absorption and operating efficiency contributed to the wider margin.

Why it is an inference: Lucky Cement does not publish a complete margin bridge showing the exact contribution from volume, coal, foreign exchange, selling prices, energy efficiency and other inputs.

What the numbers do not prove

The margin data do not prove that coal was the dominant driver.

They also do not provide a clean answer for domestic retention price because the company does not disclose enough detail to separate domestic and export net revenue per tonne with precision.

Other factors may have mattered, including:

- domestic versus export sales mix;

- product and customer mix;

- freight and distribution costs;

- inventory timing;

- power-generation mix;

- maintenance timing;

- clinker output; and

- selling-price discipline.

A disciplined reading should therefore avoid reducing the result to one sentence such as "coal fell, so the margin rose."

Why the consolidated comparison matters

The 9M FY26 comparison between the consolidated and unconsolidated margins is not just an accounting detail.

It changes the analytical question.

If the objective is to study the entire Lucky Cement group, consolidated accounts are necessary.

If the objective is to understand the Pakistan cement margin, unconsolidated accounts are the cleaner starting point.

Mixing the two can lead readers to compare unlike numbers and draw the wrong conclusion about the cement business.

Risks and what could weaken the mechanism

The margin improvement may be less durable if:

- international coal prices rise;

- the rupee weakens materially against the US dollar;

- domestic cement prices soften;

- export mix becomes less favourable;

- freight or power costs rise;

- demand weakens enough to reduce capacity use; or

- the remaining UTIS rollout is delayed or delivers less benefit than expected.

There is also a measurement risk. Public filings do not provide a full cost-per-tonne bridge, so the exact weight of each driver remains uncertain.

Falsifier

A useful falsifier is:

If fuel costs rise materially and the unconsolidated margin remains firm, then pricing mix, cost absorption or operating efficiency may be doing more of the work than the coal cycle.

The reverse also matters:

If coal benchmarks rise and the margin falls quickly despite stable volume, the improvement may have been more cyclical than structural.

Neither outcome should be judged from one quarter alone.

What to watch

-

Cost of sales as a share of net revenue

This shows whether the cost side continues to support the gross margin. -

Local and export sales mix

A change in mix can affect realised pricing and freight exposure. -

Coal benchmarks and PKR/USD

These provide directional context for imported fuel pressure. -

Confirmation on the remaining UTIS lines

Completion and company commentary may indicate whether efficiency gains are broadening. -

Unconsolidated versus consolidated reporting

Keep the cement-operation lens separate from the wider group result. -

Management's explanation of margin movement

Future filings may provide more detail on fuel, power, pricing and production efficiency.

The broader lesson

A company does not need only higher sales to produce a wider gross margin.

The quality of the improvement depends on what happened beneath revenue:

- Were costs contained?

- Did efficiency improve?

- Did the sales mix help?

- Was the currency supportive?

- Was the benefit company-specific or simply part of a commodity cycle?

For Lucky Cement, the evidence supports a balanced conclusion:

Higher local activity coincided with contained costs and disclosed operating-efficiency gains. Lower coal benchmarks were supportive external context, but they were not the whole explanation.

Sources

- Lucky Cement: Half Yearly Report for the period ended December 31, 2025

- Lucky Cement: Third Quarter Report for the period ended March 31, 2026

- Pakistan Stock Exchange: LUCK company disclosures

- International Energy Agency: Coal 2025, prices and costs

Source note: Lucky Cement filings are the primary source for company figures and management disclosures. The IEA coal series is external benchmark context, not Lucky Cement's realised coal cost.

Education & analysis, not investment advice.

Falsifier

Update this analysis if the next primary-source data point contradicts the stated mechanism.

Next data point

Monitor the next official data release, company filing, PSX notice, or sector data point linked to this mechanism.