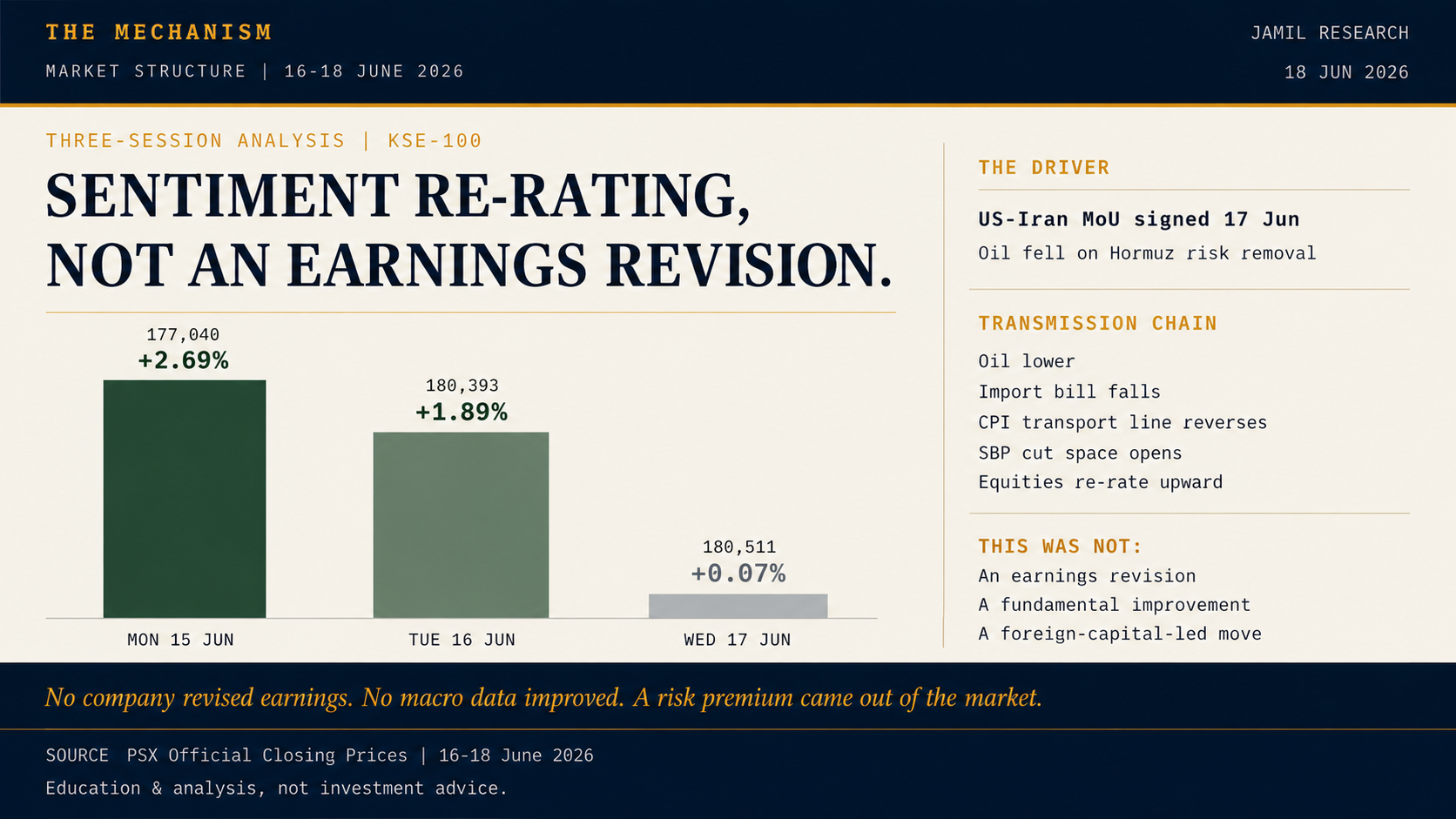

The mechanism in brief. KSE-100 moved from 172,400 on the prior Friday to 180,511 by Wednesday close. No index company revised earnings during those sessions. No macro print confirmed a structural improvement. What changed was the risk premium investors applied to Pakistan equities.

The Three-Session Pattern

The move was not a normal drift higher.

Monday closed at 177,040, up 2.69%. Tuesday closed at 180,393, up 1.89%. Wednesday closed nearly flat at 180,511, up only 0.07%.

The first two sessions did the re-rating. The third session tested the new level.

This matters because a flat day after a sharp two-day move is not automatically weakness. It can also mean the market has found a new temporary equilibrium while buyers and sellers reassess the price.

The Driver

The driver was US-Iran de-escalation and the removal of part of the oil-risk premium.

For Pakistan, the transmission chain was direct:

Oil risk premium falls → import-bill pressure eases → transport inflation can soften → SBP cut space improves → equity discount rates fall → valuations move up.

That chain does not require an earnings upgrade. It changes the multiple investors are willing to pay for existing earnings.

This is why the title matters. The move was a sentiment re-rating, not an earnings revision.

Multiple Expansion Versus Earnings Growth

An earnings-driven rally needs better earnings. A multiple-expansion rally needs lower perceived risk.

KSE-100 was trading around 6.5-6.8x forward earnings before the move, below the approximate 10-year average of 8.0x. A market at that discount does not need earnings estimates to rise in order to move higher. It can move because investors reduce the risk premium applied to the same earnings stream.

That is what happened.

The market did not decide that companies were suddenly more profitable. It decided that the macro and geopolitical risk around those profits had become less severe.

Why E&P Moved Despite Lower Oil

At first glance, E&P strength during lower oil looks strange. Lower crude is usually negative for producers.

Pakistan's E&P sector has a different local mechanism.

OGDC, PPL, MARI, and POL are not priced only on oil realisation. They are also priced on receivables, circular debt, and the probability that the government can settle energy-sector obligations. Lower oil can improve the fiscal backdrop. A better fiscal backdrop can improve the probability of receivables recovery. That narrows the circular-debt discount.

So the sector rally was not simply an oil trade. It was partly a balance-sheet and receivables-recovery trade.

The Central Assumption

The whole re-rating rests on one load-bearing assumption: oil relief must be durable.

If lower oil holds, the import bill and inflation logic can continue. If oil rebounds because the geopolitical situation worsens or supply concerns return, the multiple expansion has to be reassessed.

This is not a reason to dismiss the move. It is the correct way to monitor it.

What to Watch

The first watch item is crude oil. It is the leading variable in this thesis.

The second is OGRA fuel-price pass-through. If lower oil does not reach domestic fuel prices, the CPI channel weakens.

The third is the transport component of CPI. A visible reversal in transport inflation would confirm that the macro mechanism is moving from market expectation to actual data.

The fourth is NCCPL flow data. Domestic capital funded the initial move. Foreign participation would signal that the thesis has cleared a higher credibility threshold.

Primary source: PSX official closing prices, 16-18 June 2026.

Education & analysis, not investment advice.