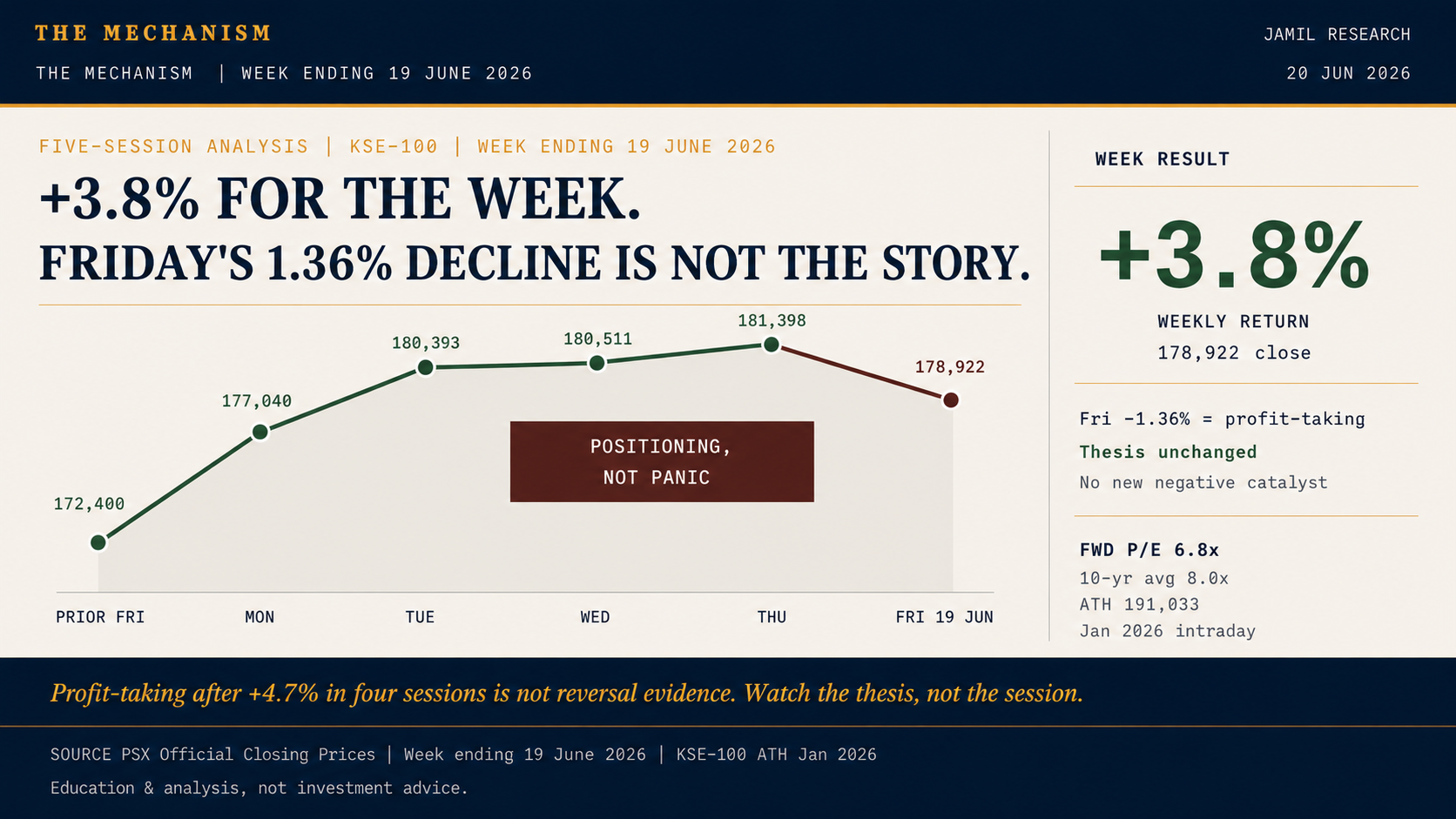

The mechanism in brief. KSE-100 still closed the week up 3.8% at 178,922.76. Friday's 1.36% decline was the final session after a sharp four-session move. The better read is positioning, not panic, unless the thesis that drove the week breaks.

Start With the Full Week

A single red session can look more important than it is.

KSE-100 closed the prior Friday near 172,400. It then moved to 177,040 on Monday, 180,393 on Tuesday, 180,511 on Wednesday, and roughly 181,398 on Thursday before closing Friday at 178,922.76.

That is still a 3.8% weekly gain.

The 1.36% Friday decline came after the market had already re-rated strongly. In that context, some profit-taking is normal. Investors who bought earlier in the week had gains to lock in. New buyers could wait for better prices. That creates a down session without requiring a new negative catalyst.

Profit-Taking Versus Reversal

The difference between profit-taking and reversal is not the index colour. It is the mechanism behind the selling.

A reversal usually needs new information. It could be an oil rebound, a policy disappointment, a weak macro print, or evidence that the original thesis was wrong.

Profit-taking only needs prior gains.

For Friday 20 June, the main thesis from earlier in the week had not been visibly broken. US-Iran de-escalation had not been reversed. The SBP's data-dependent rate path had not changed. No new macro release invalidated the inflation-and-oil chain.

That makes the session more consistent with position management than thesis failure.

Why Valuation Matters

Valuation affects how much selling a market can absorb.

At roughly 6.8x forward earnings, KSE-100 remained below its approximate 10-year average of 8.0x. The index was also below the January 2026 intraday high of 191,032.73.

A market below historical valuation can absorb profit-taking more easily than a market already at fair value. Sellers book gains, but buyers still have a valuation argument.

That does not remove downside risk. It simply means Friday's decline did not automatically change the broader setup.

What the Week Confirmed

The week confirmed three things.

First, the market was willing to re-rate when the geopolitical and oil-risk premium eased.

Second, domestic institutions were active enough to fund a meaningful weekly gain.

Third, there were buyers below the week's intraday highs. A market in real distress usually accelerates lower. A profit-taking market finds a level where buyers return.

Friday's close was lower than Thursday's level, but still materially above the prior Friday. That is the context.

What Would Change the Read

The read changes if the assumption behind the rally changes.

If oil rebounds because de-escalation fails, the market must reassess the discount-rate and inflation path. If foreign flows remain absent while domestic mutual funds reduce buying, liquidity can weaken. If the FY27 fiscal setup disappoints sectors that were bought ahead of it, part of the move can unwind.

Those are real risks. They are just not visible in the Friday headline alone.

What to Watch

The first watch item is crude oil and the US-Iran de-escalation path. The second is NCCPL weekly flow data, especially whether foreigners return and whether mutual funds sustain buying.

A further decline with no new negative catalyst can remain positioning. A decline accompanied by oil reversal, weaker flows, and breadth deterioration would be a different signal.

Until that evidence appears, Friday is best described as profit-taking after a strong week.

Primary sources: PSX official closing prices, week ending 20 June 2026; KSE-100 ATH reference, January 2026 intraday high.

Education & analysis, not investment advice.