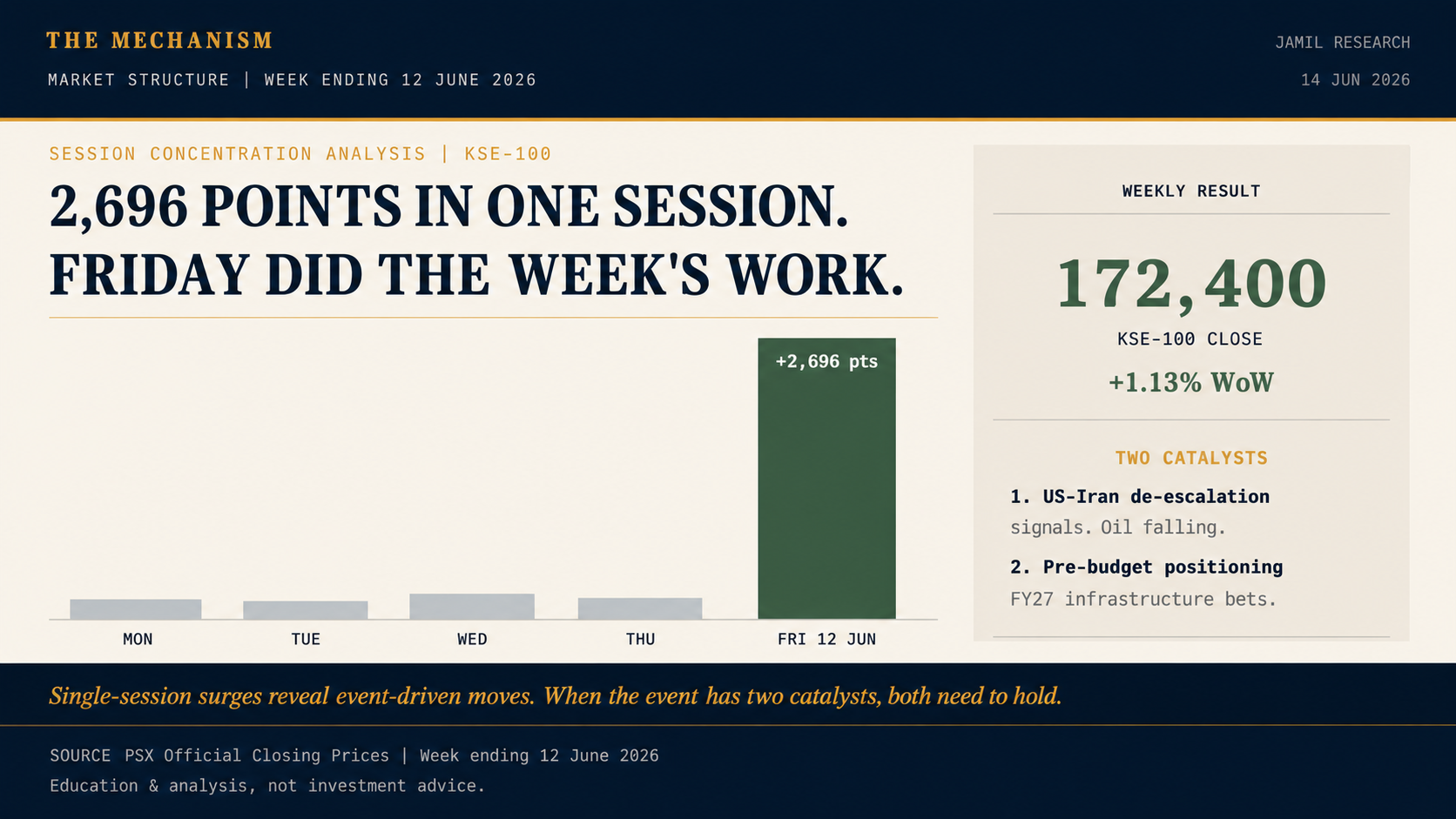

The mechanism in brief. KSE-100 closed the week at 172,400, up 1.13% from the prior Friday. The number looks modest. The structure does not. A 2,696-point Friday session did most of the work, helped by early US-Iran de-escalation signals and pre-budget positioning. That makes the move event-driven, not slow accumulation.

Why the Distribution Matters

A weekly gain can be built in two very different ways.

The first is steady accumulation. Buyers add exposure across multiple sessions, and the index climbs gradually. That kind of move usually has a broader support base because investors entered at several different price levels.

The second is session concentration. Most of the weekly return arrives in one trading day because investors react to a specific event, or to several events at once. The week ending 12 June was the second pattern.

That distinction is the real story. A concentrated move can be valid, but it is easier to reverse if the event behind it weakens. When many buyers enter on the same day and for the same reason, the same group may also reassess at the same time.

The Two Catalysts

Friday's surge had two visible inputs.

The first was early US-Iran de-escalation signalling. For Pakistan, the market transmission was simple: lower Middle East risk lowers the oil-risk premium; lower oil reduces import-bill pressure; lower fuel costs can soften transport inflation; lower inflation gives the SBP more room to cut rates; lower discount rates support equity valuations.

That is a proper mechanism. It is also conditional. It works only if the oil relief is durable.

The second input was pre-budget positioning. Investors were preparing for the FY27 budget, especially where fiscal spending and infrastructure expectations could matter. Banks, E&P names, and large groups with policy exposure all had a reason to move before the budget was actually presented.

Both inputs were legitimate. Neither was confirmed earnings improvement.

What the Heavyweights Showed

The names participating in the move were internally consistent with the thesis.

Banks such as MCB and UBL fit the rate-cut channel. If lower oil leads to lower inflation and later rate cuts, credit growth and valuation multiples become easier to justify.

E&P names such as MARI and POL fit the fiscal channel. Lower oil can ease external and fiscal pressure, which improves the probability of circular-debt settlement over time. That does not mean every E&P company benefits equally, but it explains why the sector participated.

Engro Holdings fit the pre-budget channel because several of its underlying exposures are sensitive to agriculture, fertiliser, energy, infrastructure, and fiscal policy.

The composition of the rally therefore supports the event-driven explanation. It was not random buying.

The Risk Inside the Rally

The same coherence also defines the risk.

If US-Iran tensions rise again and oil recovers, the de-escalation premium can come out of prices. If the budget disappoints on development spending or creates adverse sector treatment, the pre-budget positioning can unwind.

This is why the Friday move should not be judged only by the closing level. The relevant test is whether the two catalysts survive the next set of facts.

Valuation Context

The KSE-100 close of 172,400 still sat below Pakistan's long-run market multiple. On a forward P/E basis, the market was around the 6.5-6.8x area versus an approximate 10-year average near 8.0x.

That discount matters. It means Friday did not move the market from cheap to expensive. It moved the market from more discounted to less discounted.

But valuation discount alone is not a catalyst. A discount closes when capital believes the risk premium should fall. In this week, the market found a reason to reduce risk premium. The open question is whether that reason lasts.

What to Watch

Two items decide the durability of the move.

First, whether US-Iran de-escalation keeps oil prices soft. Second, whether the FY27 budget supports the sectors that were bought ahead of the announcement.

If both hold, Friday's surge can become the start of a broader re-rating. If either breaks, the market may give back part of the move without the underlying valuation case disappearing.

Primary source: PSX official closing prices, week ending 12 June 2026.

Education & analysis, not investment advice.