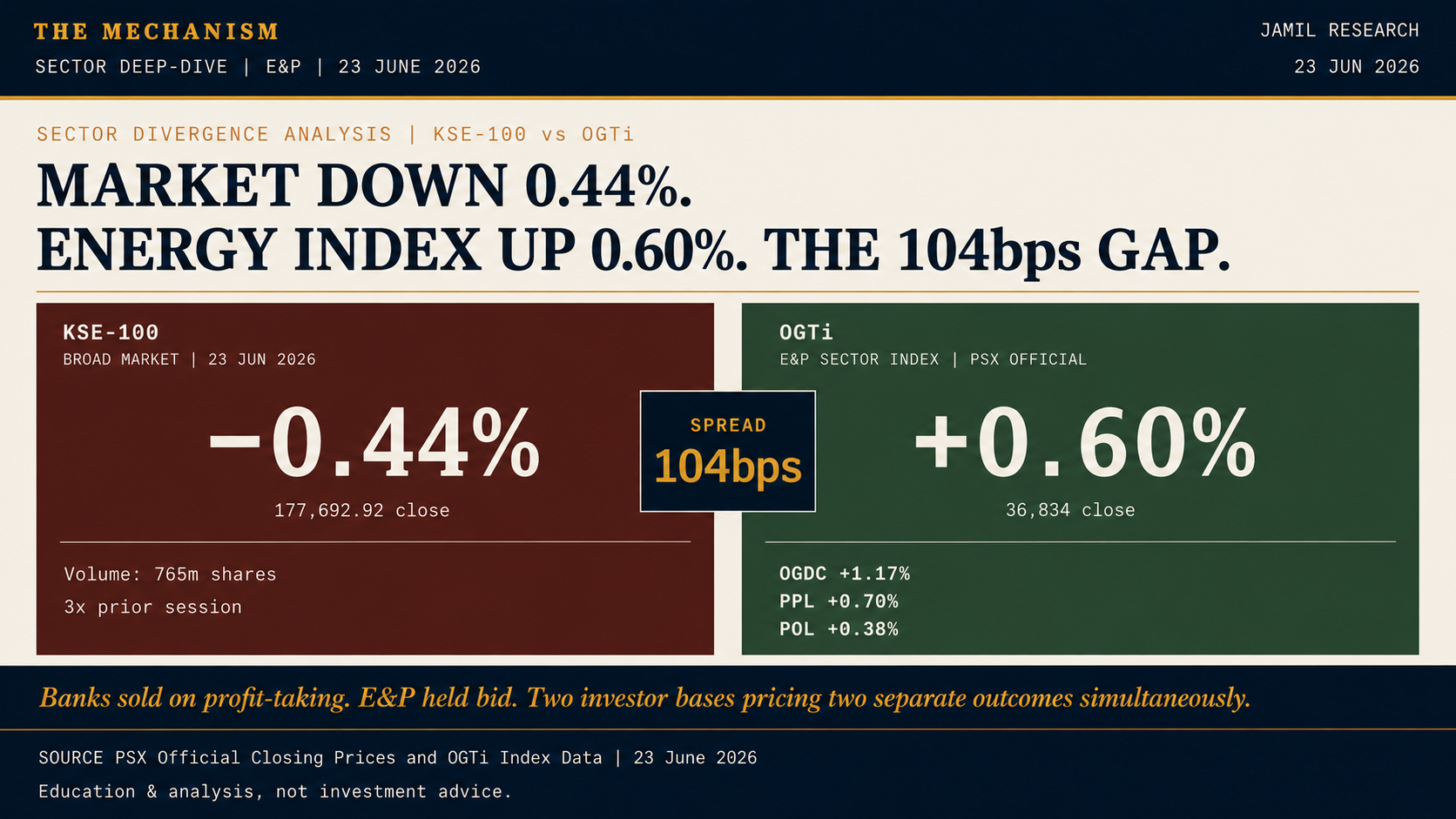

The mechanism in brief. KSE-100 closed 23 June 2026 at 177,692.92, down 0.44%. OGTi, the PSX E&P sector index, closed at 36,834, up 0.60%. The 104 bps spread was not random. It showed broad-market profit-taking while E&P continued to price a separate receivables-recovery thesis.

The Session Data

The headline numbers were mixed but clear.

| Measure | Value |

|---|---|

| KSE-100 close | 177,692.92 |

| KSE-100 move | -0.44% |

| OGTi close | 36,834 |

| OGTi move | +0.60% |

| Spread | 104 bps |

| Session volume | 765m shares |

| Advancers / decliners | 146 / 308 |

| BKTi | -1.22% |

Breadth was weak. More than two stocks declined for every one that advanced. That means the broad market was under pressure.

But the E&P index rose. That contrast is the analytical signal.

What Pulled the Market Down

Banks were a major drag. BKTi fell 1.22%.

That selling fits the prior week's flow pattern. Mutual funds had allocated heavily to banks during the week ending 19 June. After a strong move, position trimming is normal.

Bank selling in this context does not have to mean the rate-easing thesis failed. It can simply mean fund managers were reducing exposure after a quick gain.

The broad index fell because banks carry significant index weight and market breadth was negative.

Why E&P Held Bid

E&P had a different driver.

Investors buying OGDC, PPL, and POL were not pricing the same mechanism as bank buyers. The E&P thesis was more about circular debt and receivables recovery.

If lower oil improves fiscal space, the government's ability to settle energy-sector receivables improves. That narrows the circular-debt discount. This thesis was not contradicted by the 23 June session.

That explains why E&P could rise while banks fell. Different sectors were sitting at different points in their trade cycle.

Gas Names Strengthened the Signal

Gas distribution names also moved positively, with SSGC and SNGP gaining on the day.

That suggests the market was watching the gas-sector policy channel, not just upstream E&P. Gas pricing, RLNG allocation, curtailment, and circular-debt treatment all matter for the sector.

Without a specific PSX notice, the catalyst should be treated as a named inference rather than verified fact. But the price action was consistent with anticipatory positioning around the gas-sector mechanism.

Volume as Context

The session volume of 765m shares mattered.

A low-volume decline can simply mean buyers were absent. A high-volume decline means sellers were active and buyers were still present at some level.

That is closer to post-rally profit-taking than to panic. The market sold broadly, but not every sector sold. E&P found a bid.

What the Divergence Means

The 104 bps gap shows that the market was not moving as one block.

Bank investors were taking profits after a rate-sensitive move. E&P investors were still holding or adding to a receivables-recovery thesis. Both can happen in the same session.

This is why index-level commentary can miss the message. A red KSE-100 close does not mean every thesis was being rejected.

What to Watch

Three items resolve the divergence.

First, NCCPL flow data should show whether E&P continued to attract institutional buying. Second, OGRA and gas-sector policy updates should confirm or reject the gas-distribution move. Third, bank performance over the next few sessions should show whether the selling was a one-session clearing event or a deeper unwind.

If E&P continues to outperform while banks stabilize, the market is differentiating by mechanism. If E&P gives back the move and banks continue lower, the divergence was temporary.

Primary sources: PSX official closing prices and OGTi index data, 23 June 2026.

Education & analysis, not investment advice.